Fine wines, though relatively uncorrelated to traditional financial markets such as stocks or bonds, respond to macroeconomic dynamics influenced by inflation and interest rates*. Over the past decade, fine wine prices have experienced a varied relationship with interest rates, which we explain below.

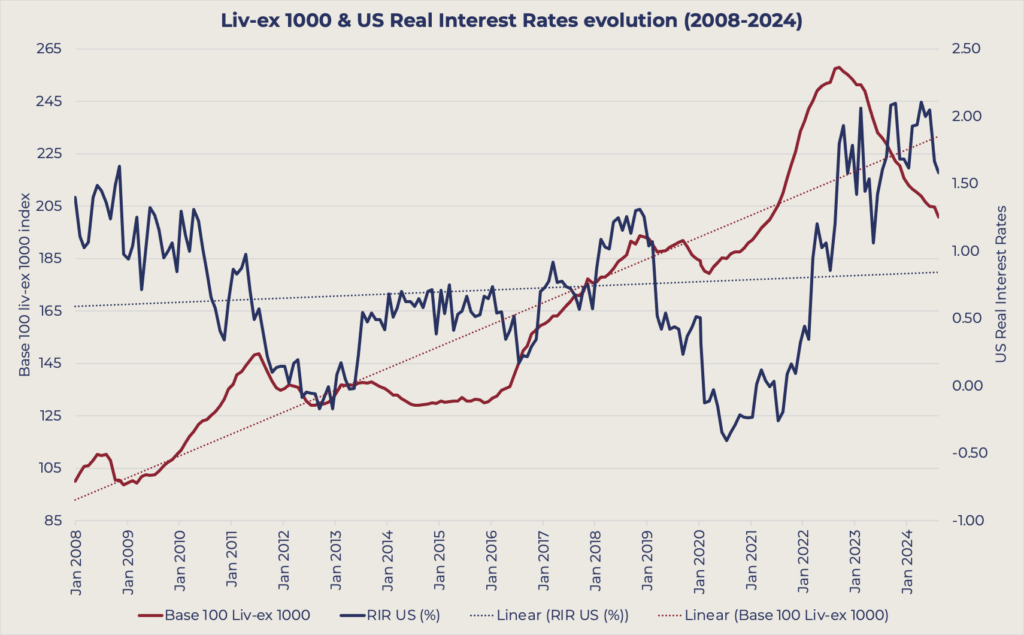

*The graph above compares fine wine price evolution based on the Liv-ex 1000 index to real US interest rates as reported by the Federal Reserve Bank. Real interest rates are calculated by adding an inflation component to the nominal interest rate. Real interest rates (RIR) can be negative, especially in periods of high inflation – the measure gives better insight into the purchasing power of a population.

To better understand the interaction between economic conditions and fine wine prices, we can examine three key phases: economic downturns, stabilisation periods, and economic growth phases.

Analysis

Economic Downturns: In times of economic crises, such as the 2008 financial collapse or the COVID-19 pandemic, central banks typically lower interest rates to encourage economic activity. Interestingly, fine wine prices tend to rise during these downturns. This countercyclical behaviour can be attributed to wine’s appeal as a safe, tangible asset, offering investors a durable and inflation-resistant investment in uncertain times.

Stabilisation Periods: Economic downturns are often followed by stabilisation phases, as seen between 2013 to 2016. During these periods, interest rates and inflation tend to stabilise, and wine prices level off or rise gently in response, reflecting broader economic equilibrium.

Economic Growth Phases: During expansionary periods, interest rates generally increase to temper inflation. Wine prices, however, respond variably depending on market conditions. For instance, between 2016 and 2019, fine wine prices rose alongside economic growth – demand in fine wine diversified amid a generally positive investor sentiment. In contrast, between 2022 and 2024, wine prices retracted despite economic growth. This is dually explained by the reduced disposable income in key markets due to high inflation, as well as a price correction for fine wine after the Covid-19 “bubble”.

Implications

In the last couple of decades, wine prices have outpaced economic growth, albeit with a trend for appreciation during periods of low or lowering interest rates. This long-term trend underlines the resilience of fine wine as a defensive asset to hold across economic cycles.

As the US Federal Reserve cut interest rates by 50 basis points in September 2024, and a further 25 basis points in November, what do we expect for the fine wine market in 2025?

If real interest rates (RIR) remain stable in 2025, we expect fine wine to follow suit. This may translate into flat prices for the majority of wines, and gentle growth for the most sought-after bottles.

If rates continue to decline, investor purchasing power will increase, and with ongoing geopolitical uncertainties, wine’s appeal as a safe-haven asset would likely rise. The current prices after a two-year reset also represent an extremely attractive entry point, further encouraging collector attention.